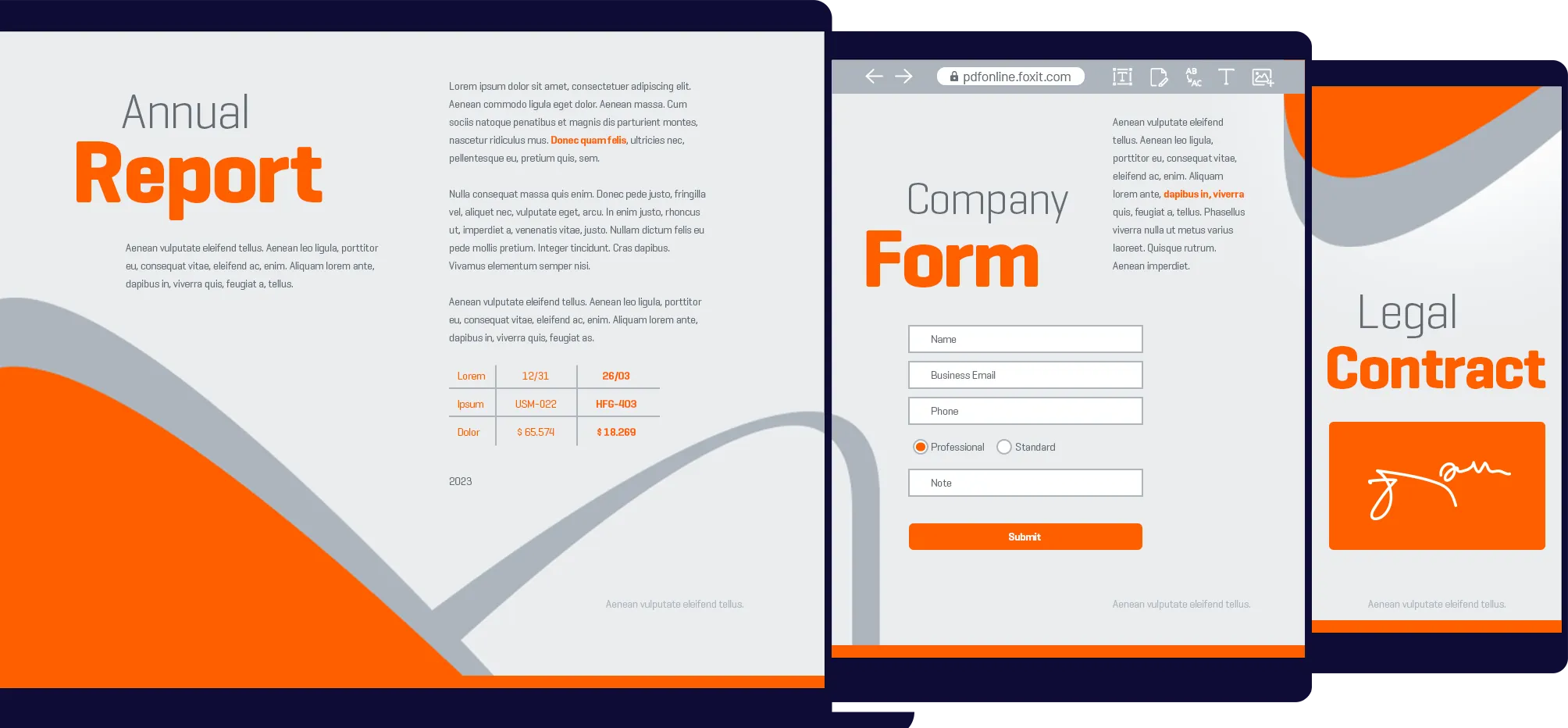

PDF Editor Suite

+

ChatGPT

Summarize. Rewrite.

Translate. Ask!

AI assistance for increased productivity.

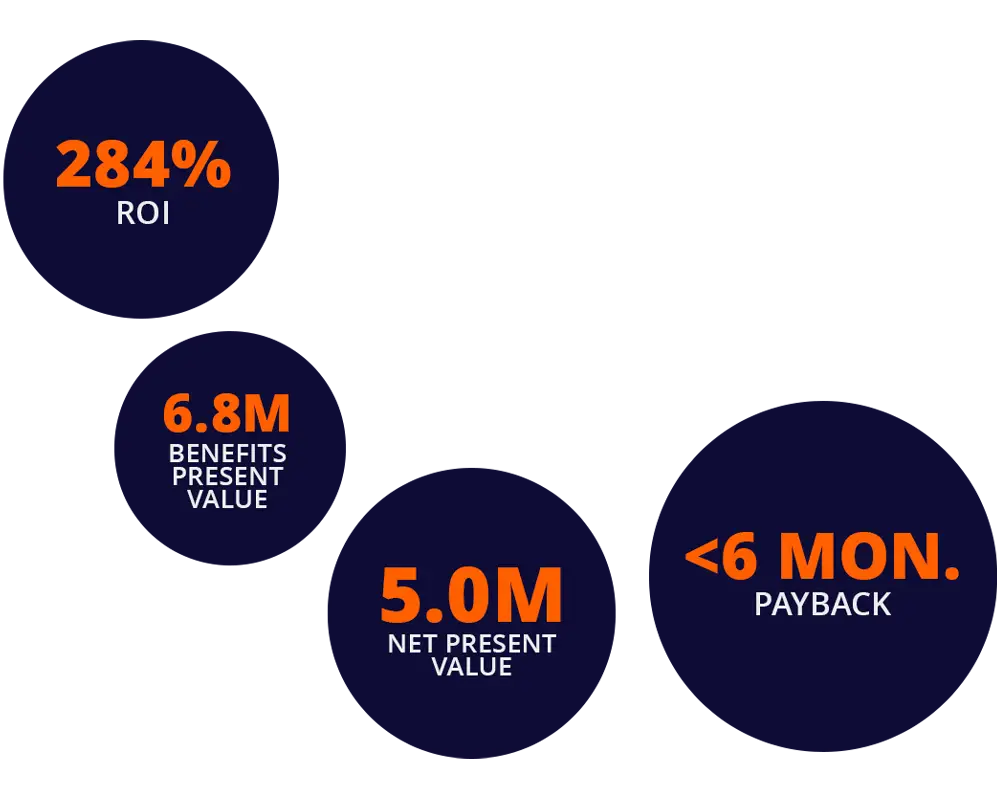

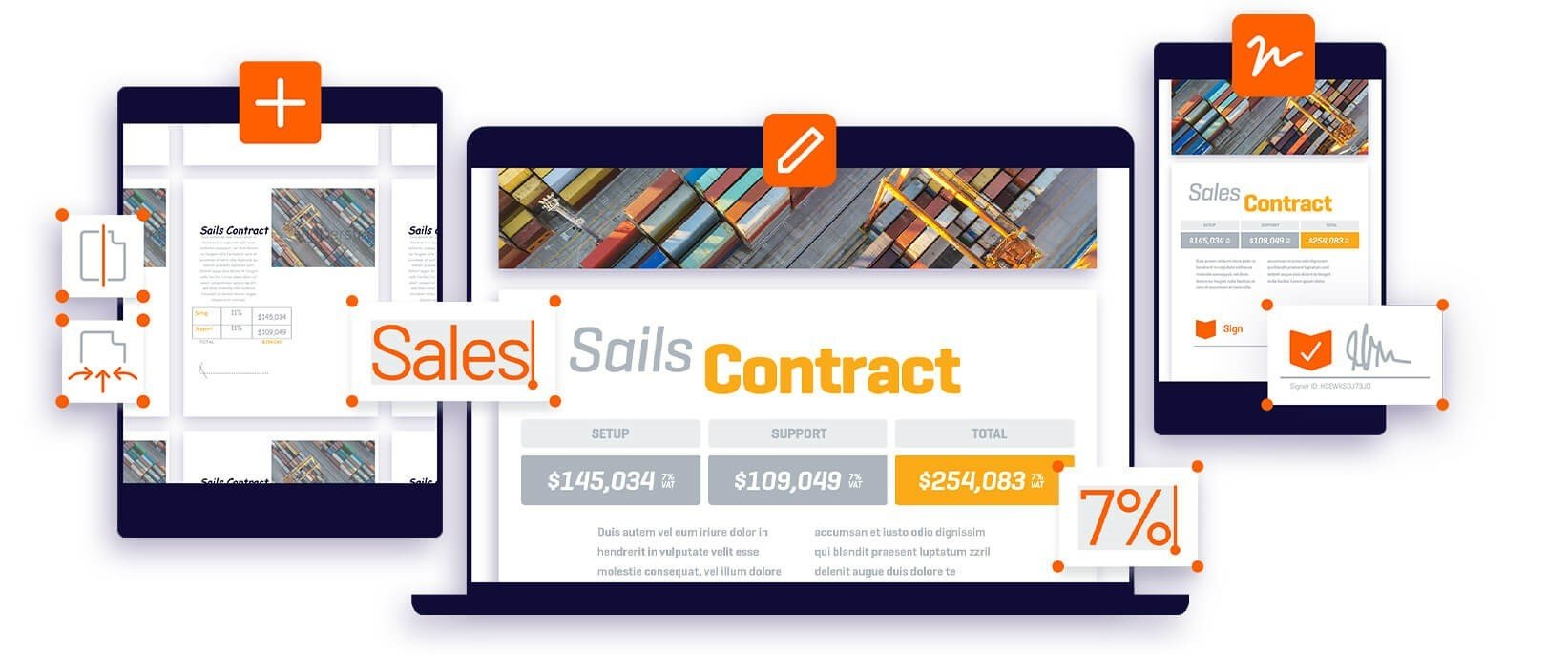

Total Economic Impact™ by Forrester®

Understand your individual 3-year ROI of switching from legacy PDF Software to Foxit PDF Editor.